Total and Permanent Disability (TPD) insurance is one of the most important protections you can have. It provides a lump sum payment if you become permanently unable to work due to illness or injury. For many Australians, this cover is held inside their superannuation fund. That can be convenient and cost-effective, but it also comes with some rules and limitations you need to understand.

This guide explains how TPD in super works, what to watch for, and why reviewing your cover is important.

What is TPD Insurance?

TPD insurance pays a lump sum if you are unlikely to ever return to work because of illness or injury. The money can be used however you need, but common uses include:

- Paying off a mortgage or other debts

- Funding home modifications or mobility aids

- Covering long-term care or medical treatment

- Creating an income stream to replace what you would have earned

In short, TPD cover is designed to provide financial security at a time when your ability to earn income has been cut short.

How TPD works in super

Most Australians first come across TPD cover through their superannuation fund. Many funds automatically include a level of life and TPD cover, with premiums deducted from your super balance.

There are some benefits to this arrangement:

- Cost efficiency – group policies can be cheaper than buying cover individually.

- Automatic cover – you may have some protection even if you didn’t actively apply.

- Premiums don’t hit your take-home pay – they are deducted from super contributions.

But there are also important considerations:

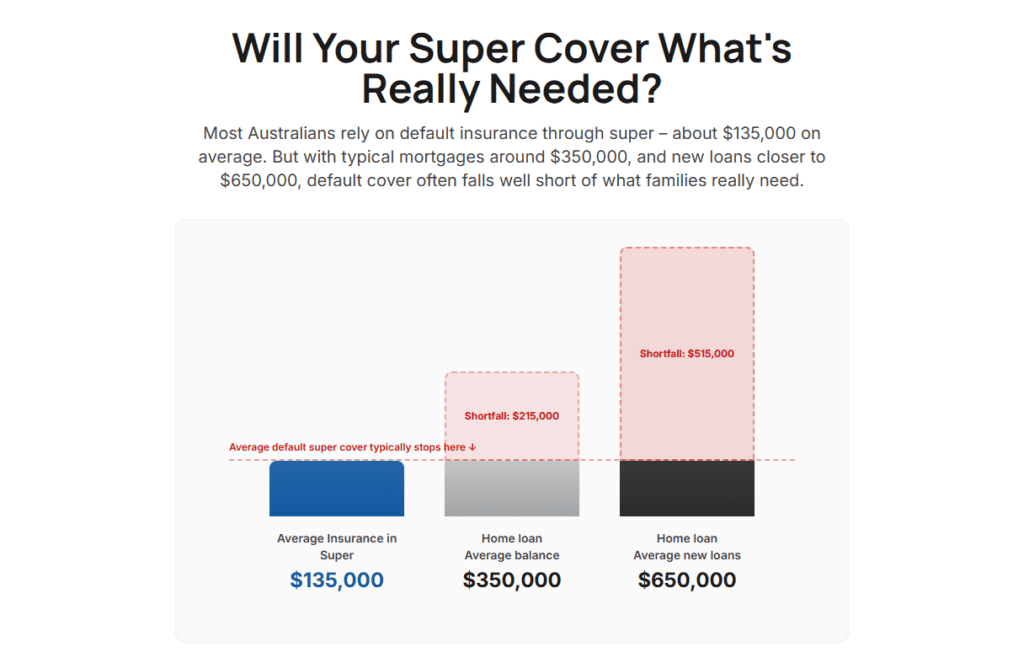

- Cover levels may be low – a default TPD amount might be $100,000–$200,000, which may not be enough to clear debts and support your family.

- Definitions matter – in super, TPD is usually based on being unable to work in any occupation you’re suited to by education, training, or experience. That’s a stricter test than policies outside super that may offer own occupation definitions.

- Release rules – even if the insurer accepts your claim, the super fund’s trustee must also approve a “condition of release” before funds are paid out. This can sometimes add time and complexity.

Tax on TPD payments from super

If your TPD policy is owned through super, the payout is treated as a superannuation benefit. This means it can be taxed, depending on your age and circumstances. For people under retirement age, a portion of the payout may be taxed before it’s released.

By contrast, TPD held outside super is generally tax-free. This difference doesn’t mean one option is always better, but it’s important to understand the impact. It’s a good idea to get professional advice before making a claim, to help minimise any tax.

Interaction with income protection

In some group superannuation schemes, receiving a TPD payment may cause income protection benefits held in the same fund to stop. This is because income protection is designed for temporary incapacity, and a TPD payout confirms permanent incapacity.

While this isn’t the case in all funds, it’s something to check in your policy documents or with your fund directly. Some people choose to hold short-term income protection inside super and add longer-term income protection outside super, so they have cover for both scenarios.

Other things to watch for

A few other considerations with TPD in super include:

- Unit-based cover – some employer or industry funds use “units of cover” that decrease in dollar value as you get older. This can mean your insurance reduces just as your family or financial commitments increase.

- Policy options vary – some funds allow you to increase or customise your TPD cover, while others have fixed default amounts.

- Trauma cover is not available – super can only hold life, TPD and income protection. Trauma insurance, which pays on events like cancer or heart attack, must be held outside super.

- Claims can take time – TPD usually requires you to be off work for at least three to six months before a claim is assessed. Combined with trustee involvement, the process can feel longer than other types of insurance claims.

Why reviewing your TPD cover matters

It’s easy to assume your super fund has you covered, but the reality is that default cover is often insufficient. Reviewing your TPD cover regularly helps ensure it matches your situation. For example:

- Have you taken on a new mortgage?

- Do you have young children or dependants who rely on your income?

- Has your income or lifestyle changed significantly?

- Are you approaching retirement, when cover inside super may automatically reduce or end?

A review can help you decide whether to top up your TPD inside super, add cover outside super, or restructure how your policies are held.

The role of advice

Not all financial advisers specialise in life (or “risk”) insurance, but those who do can add real value when it comes to TPD. They can:

- Help you work out how much cover you need

- Explain differences between cover held inside vs outside super

- Advise on ownership structures and tax implications

- Check whether your existing cover is reducing with age

- Guide you through the claims process if you ever need to use your cover

If you are speaking with an adviser, look for someone who works regularly in the risk insurance space and is comfortable explaining both the policy and the practicalities.

Final thoughts

TPD cover inside super is a useful foundation, but it’s not always enough on its own. Understanding what you have, how it works, and where the gaps may be can make a big difference to your financial security.

Take the time to check your super statement, read your fund’s insurance guide, and ask questions. If you’re unsure, seek advice. The peace of mind of knowing your cover is right for you and your family is worth the effort.