Everything you need to know to understand and choose the right life insurance protection for you and your family.

Life insurance can seem complex, but at its core it’s about providing financial protection for your loved ones if something happens to you. This guide walks through the basics and helps you understand how to find the right cover for your needs.

What is Life Insurance?

Life insurance is a contract between you and an insurer. You pay regular premiums, and in return, the insurer promises to pay a sum of money (a death benefit) to your nominated beneficiaries if you pass away.

The main purpose of life insurance is to provide financial security for your dependants. A payout can help cover:

- Immediate expenses such as funeral costs

- Outstanding debts such as a mortgage, car loans, or credit cards

- Ongoing living expenses for your family

- Future needs like children’s education

Why Consider Life Insurance?

Life insurance is especially important if you have people who rely on your income. Consider these scenarios:

- You’re the main income earner with dependent children

- You share financial obligations with a partner (such as a mortgage or loans)

- You have debts that could burden your family if you passed away

- You want funeral expenses covered so they don’t fall on loved ones

Types of Life Insurance in Australia

There are several types of life insurance, each protecting against different risks:

Life Cover (Death Cover)

Pays a lump sum to your beneficiaries if you pass away, or in many cases if you’re diagnosed with a terminal illness with less than 12 months to live.

Total and Permanent Disability (TPD) Insurance

Pays a lump sum if you become totally and permanently disabled and can’t work again. This can help cover medical costs, home modifications, debt repayments and ongoing living expenses.

Income Protection Insurance

Provides regular payments (often up to 70% of your income) if you’re temporarily unable to work due to illness or injury. Benefits are paid during the chosen benefit period, after a waiting period.

Trauma Insurance (Critical Illness)

Pays a lump sum if you’re diagnosed with a specified serious illness or injury, such as cancer, heart attack, or stroke. This money can help fund treatment and give you space to focus on recovery.

Child Cover

An optional extra on some policies. It provides a benefit if a child suffers a serious illness, helping parents manage time off work, treatment costs and other expenses without added financial stress.

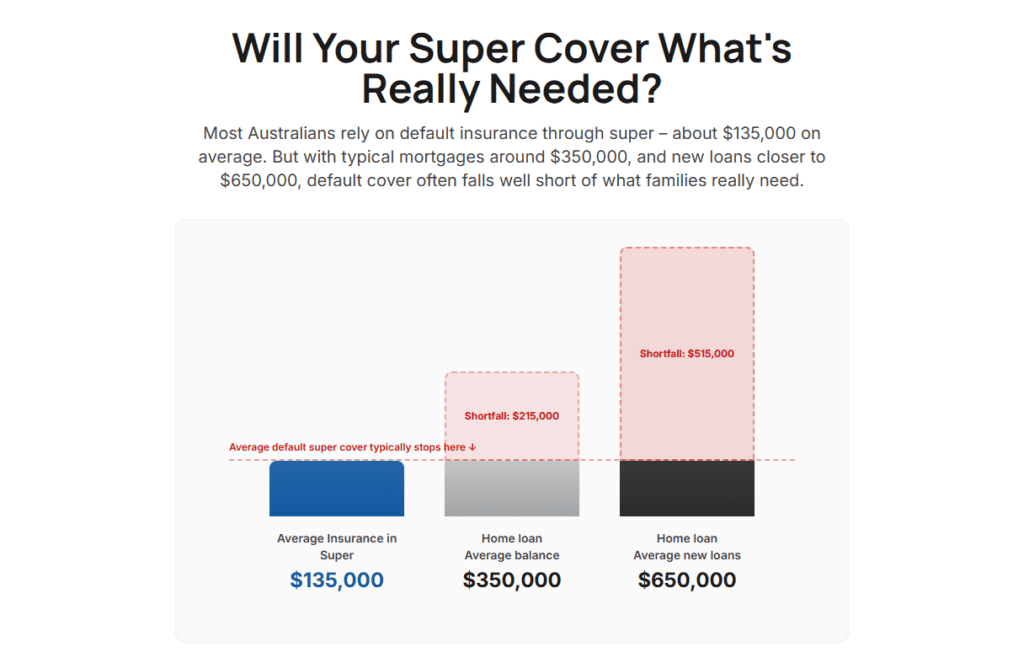

Insurance Inside vs Outside Superannuation

In Australia, you can hold life insurance through your superannuation fund or buy a policy directly from an insurer.

Inside Super:

- Often cheaper because cover is purchased in bulk

- Premiums come from your super contributions (pre-tax)

- Usually provides only basic cover with limited options

- Reduces your retirement savings

Outside Super (Retail):

- More comprehensive and customisable cover

- Claims can often be processed more directly

- Generally more expensive

- Premiums are paid from after-tax income

How Much Cover Do You Need?

The right amount depends on your circumstances, but think about:

- Outstanding debts (mortgage, loans, credit cards)

- Ongoing living costs for your family

- Future expenses (education, aged care support)

- Income replacement for a number of years

- Funeral and estate costs

- Existing assets and savings

A common guideline is 10–15 times your annual income, though your actual needs may differ.

Understanding Insurance Premiums

Your premium is what you pay to keep your cover active. The cost depends on:

- Age (cheaper when you’re younger)

- Health and medical history

- Lifestyle (e.g. smoking, high-risk hobbies)

- Occupation

- Cover amount and features

Premium Structures

There are two main types (with updated industry terms):

Stepped Premiums (now often called Variable Age-Stepped)

- Start lower but increase each year with age

- More affordable in the short term, but rise quickly over time

Level Premiums (now often called Variable)

- Start higher but stay more stable over the long term (only rising with inflation or if the insurer changes rates)

- Can be more cost-effective if you plan to hold cover for many years

Some insurers also offer hybrid premiums, blending features of both.

The Application Process

When applying for life insurance, you’ll usually:

- Research and compare options from different insurers

- Complete an application with details about your health, lifestyle and needs

- Undergo underwriting, where the insurer assesses your application (this may include medical checks)

- Receive a policy offer with terms and premium details

- Accept the policy and make your first payment

Your Duty When Applying

By law, you must take reasonable care not to make a misrepresentation. This means answering all questions honestly and accurately. If you leave out important details, your insurer could later reduce or decline a claim.

Making a Claim

If you or your family need to make a claim:

- Notify the insurer (or your adviser, if you worked with one) as soon as possible

- Provide documents, such as claim forms, medical reports, or a death certificate

- Assessment – the insurer reviews the claim and may request further information

- Decision and payment – if approved, benefits are paid to you or your beneficiaries

Most claims are paid, especially if your policy was fully underwritten at the time of application.

Working with a Financial Adviser

You can arrange insurance directly, but a qualified adviser can:

- Help you choose the right type and amount of cover

- Compare products across insurers

- Guide you through applications and underwriting

- Advocate for you at claim time