Life insurance can feel complicated and overwhelming, especially when you first start looking into it. We’ve gathered some of the most common questions people ask – and answered them in plain English, with some guidance on how to think about your needs.

What types of life insurance are there?

Life insurance usually means four different types of cover:

- Life insurance – a lump sum if you die or are diagnosed with a terminal illness

- Total and Permanent Disability (TPD) – a lump sum if you can’t ever work again due to illness or injury

- Trauma (critical illness) – a lump sum if you suffer a serious health event, like certain cancers, a heart attack or stroke

- Income Protection – a monthly payment if you’re unable to work temporarily because of illness or injury

Some people hold one or two of these, others combine them for a fuller safety net.

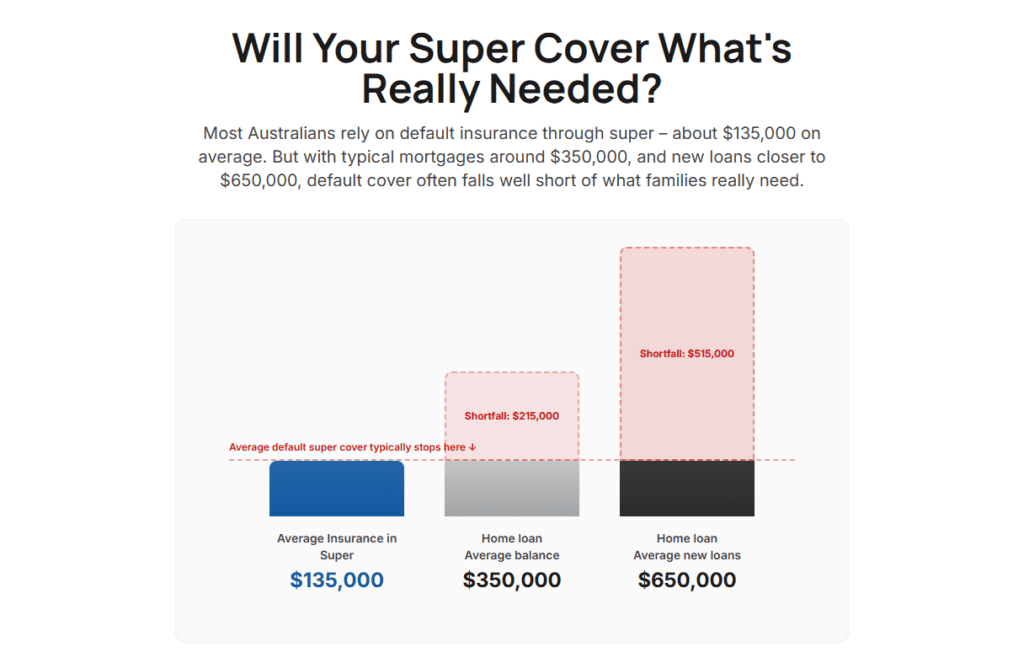

Don’t I already have insurance in my super?

Most Australians have some life and TPD cover inside their super fund. It’s a good start – but often the default amount is far too low to actually clear debts, replace income, or provide for a family.

Super cover also has stricter definitions and tax rules, so it’s worth checking:

- What type of cover you have

- How much is included

- Whether it’s enough for your situation

For many, a mix of super-based cover and extra policies outside super works best.

How much cover do I need?

There’s no single right number, but here’s a way to think about it:

- Life cover – add up debts, funeral costs, and then allow for ongoing income for your dependants. Rules of thumb like “5–10 years of income” can work, but if you have young children, a non-working spouse, or higher future expenses (like school fees), you may need more.

- TPD cover – often set at a similar level to life cover, but should also factor in costs of medical care, home modifications, or long-term support.

- Trauma cover – usually smaller, but designed to help bridge gaps in treatment costs and support you during recovery time. Many people choose $200,000–$500,000, but the right amount depends on things like your mortgage, health history, and what costs you’d want to cover if you needed time off work.

- Income Protection – usually aims to replace around 70% of your salary. Think about how long you’d need support: a couple of years, or through to retirement.

Aren’t premiums too expensive?

Premiums do increase with age, which is why reviewing regularly matters. But the cost has to be weighed against what’s at stake – for many families, even one year of lost income or an uncovered illness would be far more financially damaging than years of premiums.

Ways to keep cover affordable include:

- Adjusting cover levels as debts reduce or kids grow up

- Choosing stepped or level premiums (each has pros and cons)

- Reviewing policies every couple of years to make sure you’re not over- or under-insured

Are claims actually paid?

Yes. Despite the horror stories people sometimes hear, the reality is that more than 90% of life insurance claims in Australia are accepted. Death claims are paid over 95% of the time. Most of the small number that aren’t paid come down to exclusions, misrepresentation, or definitions not being met.

The bottom line: if your cover is set up properly and you’ve disclosed your situation accurately, claims do get paid.

When should I review my cover?

Major life changes are the trigger points:

- Buying a home or taking on new debt

- Starting a family

- Changes in income or expenses

- Marriage, separation, or divorce

- Health changes

- Approaching retirement

Even without big events, checking your cover every couple of years is a smart habit.

Do I really need all of these types of cover?

Not everyone needs everything. For example:

- Singles with no dependants may only want minimal cover for debts and funeral costs

- Parents often prioritise Life and TPD cover to protect the household

- Self-employed people may see Income Protection as vital

- Families with a history of major illness sometimes prioritise Trauma cover

The right mix depends on your circumstances, but the principle is the same: protect against the risks that would cause the biggest financial strain.

What if I don’t have an adviser?

You can go direct to an insurer or stick with super fund cover. But advisers can add real value by:

- Helping you work out how much cover you need and what type

- Explaining policy terms and differences between insurers

- Guiding you on ownership structures (inside or outside super), which can have tax implications

- Making sure your cover aligns with your overall financial plan

- Supporting you at claim time, which is often when their help matters most

Not all financial advisers specialise in life (or “risk”) insurance. Some focus mainly on investments or superannuation. If you want advice on insurance, look for someone who works regularly in this space and understands the detail of cover types, structures, and claims.

If you don’t use an adviser, you can still review cover through your super fund, or use calculators and comparison tools as a starting point. Just make sure you understand the definitions and conditions of any policy before you buy.

The bottom line

Life insurance is not about ticking a box – it’s about protecting your family and your future. Start by checking what you already have, think about what would happen if you couldn’t work or weren’t around, and review whenever life changes.

The right cover means you can face the unexpected with financial security, knowing your family has the support they need.