A closer look at what Australians are actually paying for life insurance, and what’s changing in 2026

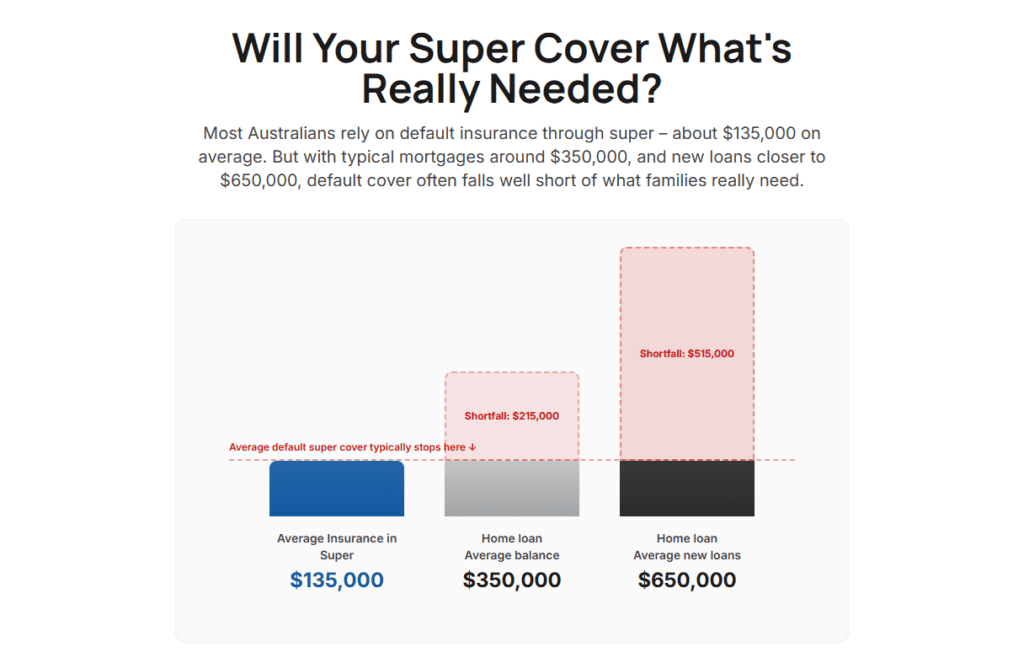

It’s a widely held belief that life insurance through your superannuation fund is the affordable option: cheaper than retail cover, convenient, and good enough for most people. For many Australians, it’s the reason they’ve never looked further.

Recent commentary in the financial press has reinforced this view, with some publications describing super fund insurance as “far cheaper” than retail cover obtained through financial advisers. It’s a claim worth examining closely. Because in 2026, for a growing number of Australians, the numbers tell a different story.

Premiums across both the retail market and the superannuation sector have been rising significantly. And for some members, the gap between what they’re paying through their fund and what’s available elsewhere has become very difficult to ignore.

What the numbers actually show

To put some real figures around this, consider a straightforward example. A male, age 45, professional occupation. $1.5 million in death cover and $1.5 million in Total and Permanent Disablement (TPD) cover, a reasonable benchmark for someone at peak earning years with a mortgage and family responsibilities.

The retail policies below are structured on a super/rollover basis, meaning premiums funded from an existing super balance with the standard 15% tax benefit already applied. This makes the comparison direct: retail inside super versus default fund cover.

AustralianSuper is used here as the super fund example because it is Australia’s largest fund by membership, has been the subject of recent commentary around insurance competitiveness, and has notified members of significant premium changes effective May 2026. It is one example only, and premium experiences will vary across funds and individual member profiles.

| Compare the difference | Annual premium |

| Retail market low (via super/rollover) | $1,306.92 |

| Retail median (via super/rollover) | $1,489.18 |

| Retail market high (via super/rollover) | $1,630.48 |

| AustralianSuper (current) | $2,240.00 |

| AustralianSuper (from 30 May 2026) | $3,000.24 |

Male, age 45, professional. Retail premiums on super/rollover basis, death + TPD. AustralianSuper based on fund calculator, Professional work rating, effective 30 May 2026.

From 30 May 2026, AustralianSuper members at this profile will be paying more than double the retail median for equivalent cover, and that retail cover can itself be held inside super and funded by rollover. The AustralianSuper increase represents a 34% jump in a single adjustment.

It is worth noting that AustralianSuper has pointed out that its rates remain lower than they were in 2022, following cuts made over the prior three years. But the current trajectory, and the gap to the retail market for members at this profile, is significant.

For female members, the picture is similar, and in some respects more pronounced. Retail insurers price female life and TPD premiums lower than male equivalents at age 45, so retail premiums via super/rollover range from approximately $1,150 to $1,457 per year, with a market median of around $1,305. AustralianSuper applies unisex pricing, meaning the same fund premiums apply regardless of gender. The gap between default fund cover and retail alternatives is wider still for female members.

Why are premiums rising?

The increases across both retail and super fund insurance reflect genuine and well-documented pressures.

TPD has been hardest hit. Mental health is now the single largest driver of TPD claims in Australia, accounting for nearly one in three payouts. In 2024, insurers paid out more than $2.2 billion in mental health-related claims, almost double the figure from five years earlier. Among Australians in their 30s, mental health TPD claims have risen by over 700% in the past decade. Insurers and super fund trustees alike have had to reprice significantly in response.

The insured pool shrank. Legislation in 2019 and 2020 cancelled default insurance on inactive accounts and removed automatic cover for younger, lower-balance members. Around five million super accounts lost coverage. With fewer members remaining insured, costs were spread more thinly, pushing premiums up for those who stayed.

Re-rating has been widespread across the retail market. Of the 16 life companies offering retail policies, 13 have re-rated at least once since 2017, and 7 have done so at least four times. APRA and ASIC launched a joint review in 2022 after a surge in consumer complaints, finding that some increases were not applied in accordance with policy terms. TPD and disability premiums rose an estimated 38 to 48% over three years across the retail market, according to KPMG industry analysis.

These are market-wide forces. No single insurer or fund is immune, and the pressures are not going away quickly.

Can retail policies actually be held inside super?

This is something many people don’t realise, and it changes the nature of the comparison considerably.

Retail life insurance policies from a range of established Australian life insurers can be owned by a superannuation trustee and funded by rolling over money from your existing super fund. When structured this way, the fund claims the premium as a tax deduction and passes the 15% tax saving back to your account, effectively reducing the net cost from your balance.

This means the choice is not simply between your default super fund cover and paying out of pocket for a retail policy. A third option exists: tailored retail cover, with full product choice, held inside super and funded from your super balance.

There are considerations involved in this structure, including implications for TPD claim taxation below preservation age and beneficiary nomination rules, which are worth working through with an adviser. But the option itself is real and widely used.

Three questions worth asking

If you hold insurance through a super fund, and most working Australians do, these are worth considering:

Has your fund notified you of upcoming changes? Some of Australia’s largest funds have communicated material premium changes effective mid-2026. These notices typically arrive by email or through member portals and can be easy to overlook. The increases can be significant.

Do you know your work rating? Super funds categorise members by occupation risk. Many members have never updated their work rating since joining the fund and may be paying a higher rate than their occupation warrants.

Is your default cover actually right for you? Default cover is designed for convenience, not precision. For many members it is either insufficient for their actual needs or more than they require. Neither situation is ideal, and because premiums are deducted from super rather than from take-home pay, many people simply don’t notice.

What a specialist adviser can do

A risk insurance specialist offers something that reviewing your super statement alone does not: access to the full market, and the expertise to assess not just what you are paying but what you are actually covered for.

Beyond premium comparisons, structure matters. Super fund income protection is typically limited to a two-year benefit period. Retail policies can cover to age 65. Super fund TPD cover generally requires you to be unable to work in any occupation, a much higher bar than the “own occupation” definition available through retail policies. These differences can determine whether a claim succeeds or fails.

An adviser can benchmark your current cover, identify whether the structure suits your needs, and present alternatives, including options that remain inside super if that is your preference. Many offer an initial review at no cost.

The bottom line

Life insurance through super is convenient, and for many Australians it provides a valuable safety net. But convenience is not the same as value, and “inside super” is not the same as “best available.”

With premiums rising across the market, 2026 is a good year to take a closer look at what you have, what it costs, and whether there is a better option. The numbers may surprise you.

This article contains general information only and is intended for illustrative purposes. It does not take into account your personal financial situation, needs, or objectives. The premium comparison shown is based on a specific example profile and should not be taken as representative of your own circumstances or as a recommendation for any particular product or course of action. Before making any decision about your insurance cover, you should consider your own situation and obtain advice from a licensed financial adviser who can assess your individual needs. Life insurance products referred to in this article are subject to the terms, conditions, and eligibility criteria of the relevant product disclosure statements.

Sources: APRA/ASIC joint review of life insurance premium practices (2024 to 2025); KPMG Life Insurance Industry Insights 2023; Council of Australian Life Insurers mental health claims data 2024; ASFA research paper on insurance in superannuation 2024; AustralianSuper insurance calculator (March 2026); retail premium comparison data via LifeRisk Online (March 2026), super/rollover basis. Premium comparison: male, age 45, professional, $1.5m death + $1.5m TPD.